- Weekly Metals Mining Rundown - Free

- Posts

- Weekly Metals Mining Rundown for Week Ending 4 July 2025

Weekly Metals Mining Rundown for Week Ending 4 July 2025

Most metal prices and mining stocks rose this past week, with precious metals standing out

Host Rock Capital

July 04, 2025

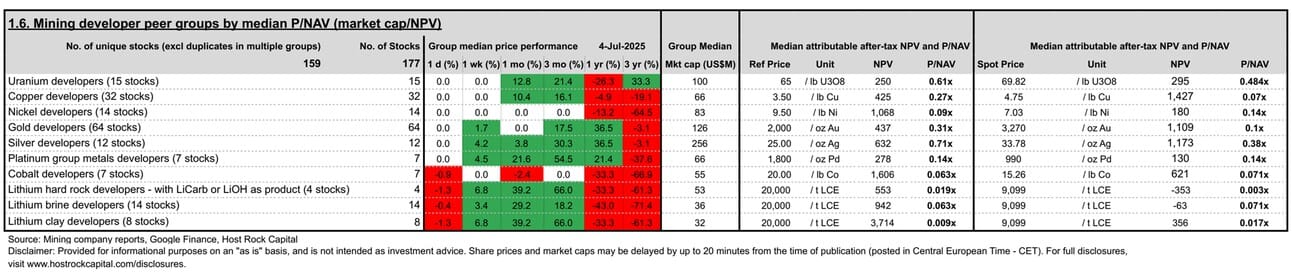

This past week’s top & bottom metal price and mining company peer group movers include:

This past week’s top 40 performing metals mining stocks (out of Peer Table’s 473) include (share price rounding errors apply, as sourced from Google Finance):

Covered metals mining company announcements incorporated into this week’s Peer Table (resource updates, economic studies, changes in project ownership) include:

3 July 2025 (intraday) - Gold developer Spanish Mountain Gold (TSXV:SPA) announced results of a PEA for its flagship Spanish Mountain gold project in BC, Canada, which included several changes compared to the prior 2021 PFS, including: larger project scale (now 26 ktpa, was 20 ktpd), improved flowsheet, optimized open pit slopes, upsized power to accommodate future electrification of equipment, filtered/dewatered tailings, and an updated/tightened resource estimate including main deposit Measured and Indicated resources of 292Mt @ 0.44 g/t Au for 4.2Moz Au + Ag credits (total resources are down slightly to ~4.7Moz AuEq). After-tax NPV5% was C$1.0b at US$2,450/oz from initial capital costs of C$1.25b (including $259m project contingency), or at our estimated 3-month trailing average gold price of $3,270/oz NPV was down slightly to US$1.6b. SPA stock traded flat +0% on 3 July intraday following this news (vs. our 67-company gold developer group median that had also been flat +0%), before finishing the week (ending 4 July) up +5.9% (vs. group median +1.7%) to a market cap of C$80m, market cap/oz resource of US$12/oz AuEq (vs. group median $38/oz AuEq) and P/NAV (market cap/post-tax NPV) of 0.035x (vs. group median 0.10x) based on NPV of US$1.67b that was down slightly from old 2021 PFS - at our estimated 3-month trailing average metal prices (US$3,270/oz Au.)

1 Jul 2025 - Gold developer Santana Minerals Ltd (ASX:SMI) announced updated PFS results for its flagship Bendigo Ophir project in New Zealand, which adopted a staged and more selective mining strategy compared to the larger-scale, more generalized operation assumed in the 2024 PFS that included more aggressive pre-stripping. Average open pit mill feed in the new study was up 15% to 2.53 g/t Au. Resulting economics were similarly strong as 2024 PFS, with reported after-tax NPV6.5 of A$780M at A$3,500/oz (30% below current price) from pre-production capital of only A$277m (was A$302m). According to the sensitivity of the NPV to metal prices provided in then study, the project NPV went down slightly at our Reference gold price of US$2,000/oz and up slightly at our estimated 3-month trailing average gold price of US$3,144/oz. SMI stock traded up slightly on Canada Day 1 July 2024 following this announcement, before closing week (ending 4 July) up +1.9% (vs. our 67 gold developer median up +1.7%) to a (4 July) share price of A$0.56, a market cap A$397m, market cap/oz resource of US$111/oz Au (near upper-quartile range of gold developers), and P/NAV (taken as market cap/after-tax NPV) of 0.26x (similarly near upper-quartile range) with premium appearing to be attributed to the strong economics (from high open pit grade of 2.53g/t and high NPV to capex ratio)and the fairly advanced PFS stage of the project with permitting studies underway, making SMI a good take out target, ether for intermediate gold producer OceanaGold Corporation Gold (TSX:OGC) that has producing mines in New Zealand already and trades much higher at US$275/oz AuEq resource, or for another producer looking to break into emerging mining jurisdiction of New Zealand.

30 June 2025 - Gold explorer Redcastle Resources (ASX:RC1) announced a resource update for its Queen Alexandra and Redcastle deposits that more than tripled total resources to a still rather small 42 koz Au, grading high for an open pit resource at 2.7 g/t, and this includes a pit-constrained 26 koz @ 2.5g/t Au. RC1 also stated that the estimate provides excellent models for further resource delineation, including below the open pit conceptual shells and at other prospects within the Redcastle Project East West fairway. RC1 stock traded flat on 30 June +0%, before closing week flat also +0% at A$0.007/sh and a market cap/oz resource of US$6.5/oz - a ~74% discount to our 90-company gold explorer peer group median US$25/oz.

30 June 2025 - Gold explorer Gateway Mining (ASX:GML) announced the acquisition of the Yandal gold project (with 400koz resource) from fellow gold explorer Strickland Metals Ltd (ASX:STK) for A$45m in GML shares (1.5b shares), such that STK will own roughly 79% of GML stock. This more than quadruples GML’s shares, and nearly double its resource ounces to 0.91 Moz, and importantly includes an active mining license application for Horse Well resource of 291.5koz that has multiple toll treating option in the region. STK is opting to distribute/issue 80% of these GML consideration shares directly to STK shareholders. GML stock traded flat +0% on 30 June following this news on strong volume (vs. gold explorer median of down -2%), before closing the week flat +0% at A$0.027/sh (vs. group median +0%), market cap A$57m (pro-forma assuming 1.9b GML shares out) and (pro-forma) market cap/oz resource of US$41/oz - in between our gold explorer median and mean US$25/oz and US$55/oz. STK stock also traded flat +0% on 30 June vs. peer group median down -2%, before closing week (ending 4 July) up +7.1% (vs. group median flat +0%) to A$0.15/sh, market cap A$351m and a market cap/oz resource US$33/oz (including, for now until distributed to shareholders, STK’s entire proposed ~79% equity stake of GML’s 0.91 Moz, which is more than the 400koz it divested with Yandal) - just above median $25.4/oz and still well below mean US$56/oz.

30 June 2025 - Gold developer Ausgold Limited (ASX:AUC) announced DFS results along with a resource update for its flagship Katanning project in Western Australia, further de-risking the open pit mine plan and paving the way for front-end engineering and project financing. Post-tax NPV5 was A$954m (US$0.62b) at A$4,300/oz (US$2,795/oz) from pre-production capital of A$355m (US$231m) and the updated resource was 2.44 Moz grading 1.11g/t (reserve of 1.25Moz also grading 1.11g/t). Encouragingly, the resource grade improved by 5% on an optimized resource pit shell and overall tighter estimate that resulted in contained resources ounces falling by nearly 20%. Project engineering and economics also appears tighter as the NPV came up some short of that of the 2022 PFS (at apples to apples gold prices). This led to AUC trading down -16% on 30 June, before closing the week (ending 4 July) down -15% at A$0.64/sh (vs. our 67-company gold developer median daily performance up +1.7%), a market cap of A$227m (US$149m), and a market cap/oz resource of US$61/oz - in between gold developer group median $38/oz and mean $65/oz - for this advanced feasibility stage, near shovel-ready project (pending permitting completion and project financing). On P/NAV (taken as market cap/post-tax NPV), AUC trades at 0.17x - in-line with group mean 0.16x - both at our estimated 3-month trailing average gold price of US$3,270/oz.

30 June 2025 - Gold developer Brightstar Resources (ASX:BTR) announced a DFS for its 100%-owned Menzies and Laverton gold projects in Western Australia, where large-scale mining is set to begin in early 2026 through a targeted ore purchase agreement at nearby Paddington mill for which there is an existing memorandum of understanding. The study targeted an initial (small subset of resources) 6.4 Mt @ 1.81 g/t Au for 0.34 Moz recovered, outlining a pre-tax NPV5 of A$203m at A$4,500/oz from pre-production capital of only A$14m (as ore is to be initially processed off-site Paddington mill in 2026 before a 1mpta is due to be constructed in 2027 for expansion capex of A$204m on existing mill site). BTR stock traded down -9% on 30 June (vs. gold developer median +0%), before closing the week (ending 4 July) down +4.1% (vs. group median up +1.7%) - perhaps because this study excluded much of BTR’s attributable resources amounting to more than 3Moz across the broader containing Menzies, Laverton, and Sandstone hubs making up this newer flagship project - most of which are left as future upside to supplement these study economics. BTR trades at market cap A$220m at A$0.47/sh and market cap/oz resource of US$44/oz Au - in between our 67-company gold developer group median and mean of US$38/oz and $65/oz AuEq (and a ~75% discount to where our intermediate gold producer median of US$163/oz - where BTR aims to graduate to with commencement of large-scale production by next year according to this DFS). On P/NAV (market cap/70% of reported pre-tax NPV), combining the company’s 2024 Scoping Study for other earlier stage project Jasper Hills and this DFS for Mezies/Laverton, BTR trades at 0.45x at 3-month trailing average US$3,270/oz - well above our gold developer mean of 0.16x at same gold price, but well below the ~1x range BTR is headed towards if it graduates to become a large-scale gold producer as planned.

30 June 2025 - Gold developer Barton Gold (ASX:BGD) announced a resource update for its South Australian Challenger gold project that grew project resources to 223 koz @ 0.72 g/t. The update focused on higher-grade tailings and open pit materials, and grew company wide South Australia resources by 9% to 1.90 Moz AuEq (98% from Au, rest Ag).

30 June 2025 (after-market) - Gold developer Barton Gold (ASX:BGD) announced the acquisition of the 279 koz for payment of A$5.5m made in 2 stages, including A$0.5m cash and A$5m in stock at a recent VWAP of A$0.78, in addition to a contingent benefit of up to A$9.5m in cash conditional on future gold production. The acquisition grows BGD’s South Australia resources by another BGD’s proforma shares now in include additional 6.4m pending shares for this transaction, for proforma shares of 229.6m. BGD stock closed week (ending 4 July) up +1.3% (in-line with group median +1.7%) to proforma market cap of A$184m at 30 June closing price of A$0.80/sh, for a lowered) market cap/oz resource of US$55/oz (which is now slightly lowered from bot this resource upgrade and acquisition) - in between our 67-company gold developer peer group median and mean US$38/oz and US$65/oz. Similarly on P/NAV (market cap/70% of reported pre-tax NPV), BGD trades at 0.19x according to results of its 2025 optimized scoping study for only its Tunkilla project (just above group mean 0.16x) - both at our recent trailing average gold price of US$3,270/oz, with a feasibility being completed this year and stage 1 production due as early as late 2026.

Disclaimer: Provided for informational and educational purposes, and is not intended as investment advice. For full disclosures, visit www.hostrockcapital.com/disclosures.