- Weekly Metals Mining Rundown - Free

- Posts

- Weekly Metals Mining Rundown for Week Ending 6 Mar 2026

Weekly Metals Mining Rundown for Week Ending 6 Mar 2026

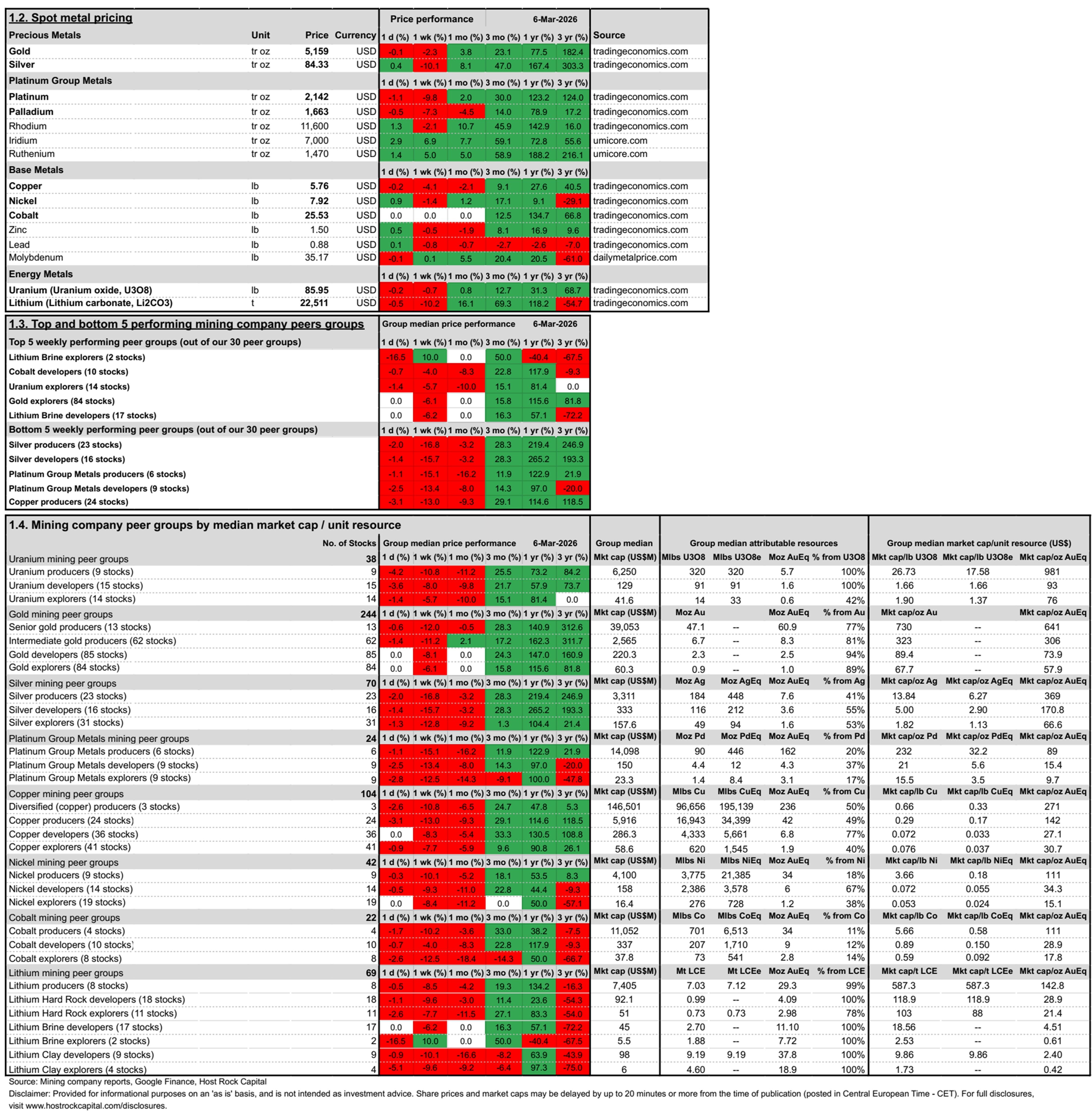

Metal prices dropped this past week, led by lithium, silver, and platinum falling -10% apiece to $22,500/t Li carb, $84/oz Ag, and $2,140/oz Pt; Copper and gold also dropped, by -4% and -2% to $5.75/lb Cu and $5,150/oz Au; This led to most mining stocks tanking by -8% or more, led by silver and PGM miners mostly dropping by -13% or more; Covered announcements include PEA for Hat project in BC by Doubleview Gold Corp, the acquisition of Arizona Sonoran Copper by Hudbay Minerals, and an updated PEA and MRE for Cerro Caliche by Sonoro Gold Corp.

Host Rock Capital

March 08, 2026

This past week’s top & bottom metal price and mining company peer group movers include:

6 Mar 2026

This past week’s top 40 performing metals mining stocks (out of Peer Table’s 504) include (share price rounding errors apply, as sourced from Google Finance):

Covered mining company announcements incorporated into this week’s Peer Table (resource updates, economic studies, changes in project ownership):

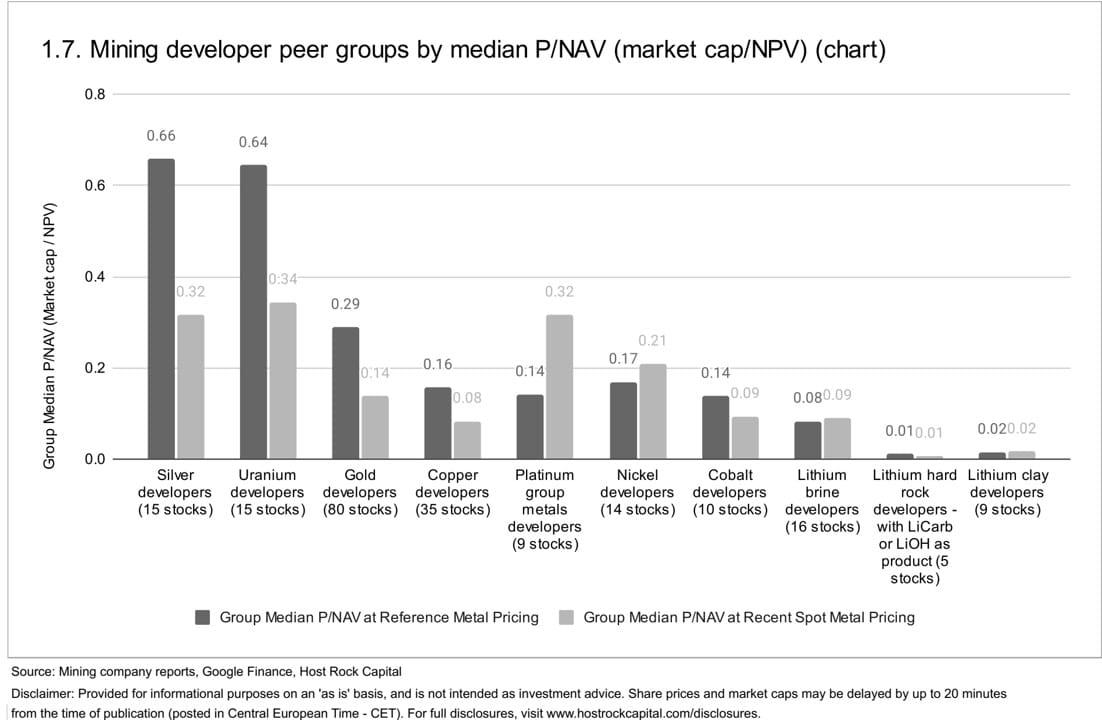

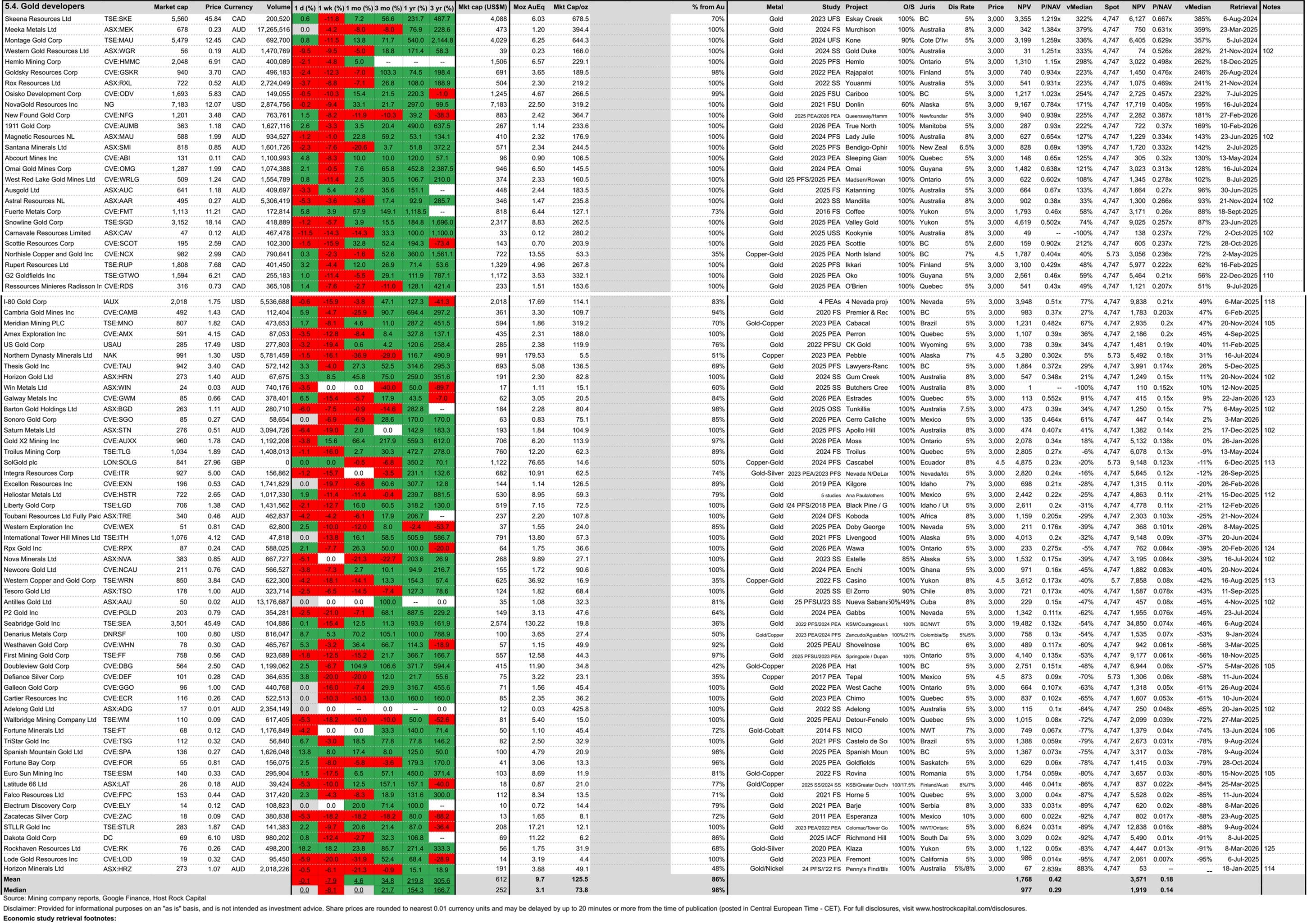

Former gold and copper (and cobalt) explorer – now developer – Doubleview Gold Corp (TSXV:DBG) announced Monday (2 Mar) a maiden PEA for its flagship Hat project in the Northwestern reaches of Canada’s western-most frontier of British Columbia. The study’s base case (A1 scenario) yielded a post-tax NPV of C$4.96b at consensus metal pricing of $3,272.60/oz Au and $4.88/lb Cu, from initial capital of C$3.55b. And this NPV: (a) increases to C$11b at spot metal pricing US$5,200/oz Au and $6.00/lb Cu, (b) assumes conservative metal recoveries of 66% for Au and 80% for Cu according to past test work, which are expected to be improved to 75% for Au and 89% for Cu (increasing the NPV to C$6.7b at consensus metal pricing or C$13.5b at spot prices, as shown under the PEA’s A2 scenario), (c) excludes a possible scandium circuit (which the PEA shows improves the NPV marginally under scenario B). DBG stock dropped -7% (in-line with Cu developer median -8%) over past week (ending 6 mar), to C$2.50/sh or market cap C$564m, with Hat’s large resource base of 11.9Moz AuEq or 9.9 Blbs CuEq (50% Au, 42% Cu, 6% from Co, rest Ag - excluding Hat’s Scandium resources) trading at a market cap/oz resource of US$35/oz AuEq ($0.042/lb CuEq) for a 53% discount to gold developer group median $74/oz AuEq. And according to the separate metal price sensitivities provided in the PEA for Cu and Au (for the conservative A1 scenario), DBG now (4 Mar) trades and a P/NAV (market cap/NPV) of 0.060x at 3-month trailing average metal pricing of US$4,747/oz Au and $5.73/lb Cu – a 57% discount to our gold developer group median 0.14x at same $4,747/oz Au and a 28% discount to our copper developer group median 0.08x at same $5.73/lb Cu.

6 Mar 2026

6 Mar 2026

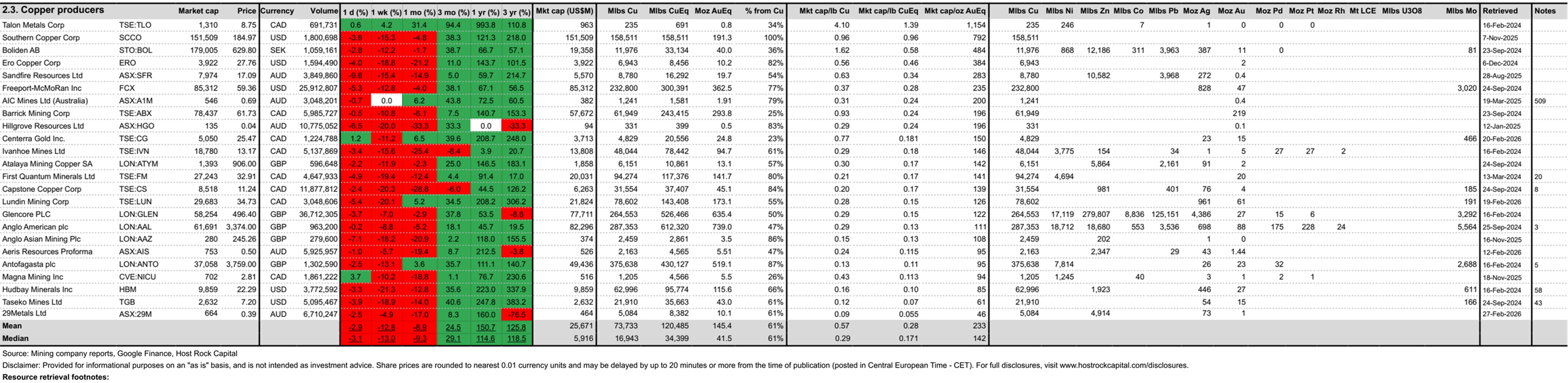

Copper producer Hudbay Minerals Inc. Minerals (NYSE:HBM) announced Monday (2 Mar) the acquisition of copper developer Arizona Sonoran Copper Company Inc. (ASCU:TSX | ASCUF:OTCQX) and its large pure-play copper Cactus project in Arizona, which hosts resources of 12.7 Blbs Cu, and has a 2025 PFS that yields a post-tax NPV of US$4.36b at our estimated 3-month trailing average copper price of $5.73/lb – translating to a (4 Mar) ASCU P/NAV (market cap/NPV) of 0.26x AFTER ASCU stock gained +1% over past week ending 6 Mar (in-line with 34-company copper developer group mean 0.27x and above median 0.08x at same copper price). And importantly, this acquisition will create the third largest copper district in North America together with Hudbay’s existing Copper World project (also in Arizona), with expected annual copper production of 92,000 t Cu (203 Mlbs Cu) from 2030 – some time after which Cactus is now due to add another 103,000 t Cu per annum (227 Mlbs Cu). Together with HBM’s other near-term optimization projects, this deal provides HBM with a clear pathway to more than double its overall copper production from ~125,000 t Cu per annum now (275 Mlbs Cu) to over 250,000 t Cu annually (551 Mlbs Cu) by 2030 from Copper World, and ultimately to 350,000 t Cu per annum (771 Mlbs Cu) from Cactus (~2.8x HBM’s current Cu production levels). HBM will issue 0.242 sh HBM per share ASCU in all-stock deal, valued at C$9.35/sh ASCU for 30% premium to prior close and 36% premium based on both HBM and ASCU’s 20-day VWAP. HBM’s basic shares will increase by ~11.5% to ~442.3m to acquire the remaining 90.1% of ASCU shares outstanding (HBM already owned 9.9%), to grow its mineral resource inventory by ~14% to 95.8 Blbs CuEq (115.6 Moz AuEq) – 66% from Cu, 24% from Au, 7% from Ag, rest Zn (by increasing HBM’s attributable ownership of ASCU’s resources from 9.9% to 100%). HBM’s stock dropped -21% over past 5 trading days (just underperforming our 24-company copper producer median drop of -13% for same period) to US$22.29/sh, proforma market cap US$9.8b, (proforma) market cap/lb US$0.10/lb CuEq ($85/oz AuEq) – a 40% discount to Cu producer group median US$0.17/lb CuEq ($142/oz AuEq).

6 Mar 2026

28 Feb 2026 - Gold developer Sonoro Gold Corp (TSXV:SGO) announced the results of an independent updated mineral resource estimate (MRE) and an updated PEA on its flagship Cerro Caliche gold project in Sonoro, Mexico. The study contemplated a 10-yr, 16 ktpd open pit and heap leach operation. Mineral resources increased by 73% to 0.83 Moz AuEq (85% Au/15% Ag) according to our retrieved numbers, which helped increase production rates compared to the 2023 PEA. And although this 2026 study’s somewhat larger mine plan with higher production rates did not quite offset cost inflation since the 2023 study (NPV fell slightly by ~5% at our 3-month trailing gold price $4,747/oz), this MRE and PEA was reported to reflect less than 30% of the known mineralized zones on the Cerro Caliche concession that was recently nearly tripled in size - so the potential for future expansion of the proposed mine in both capacity and mine life is considered favorable (as management reports). Post-tax NPV is US$447m at our estimated 3-month trailing average gold price $4,747/oz Au, which is slightly (~5%) below the 2023 PEA result (according to metal price sensitivities provided in the studies), and yields a similar P/NAV of 0.14x at 27c/sh (in-line with 77-company gold developer group median 0.14x at same $4,747/oz Au) - after SGO stock dropped -7% over past week ending 6 Mar (in-line with group median drop of -8%), to 27c/sh, market cap C$85m, market cap/oz resource US$75/oz AuEq (in-line with group median US$74/oz). The study’s reported post-tax NPV was US$224m at gold price US$3,500/oz from initial capital of only US$83m including $11m contingency (heap leach does not require a costly mill) with fairly low AISC of US$1,902/oz (mid-range AISC seems to have risen in recent years from the ball park of ~US$1,500/oz to ~$2,000/oz - reflecting gold prices of $3,000/oz and $4,000/oz according to the rule of thumb that AISC should be one-half of the gold price in the long term).

6 Mar 2026

Disclaimer: Provided for informational and educational purposes on an ‘as-is’ basis, and is not investment advice. For full disclosures, visit www.hostrockcapital.com/disclosures.